JANUARY 2026 PERFORMANCE

")

JANUARY 2026 PERFORMANCE

| MARKET COMMENTARY |

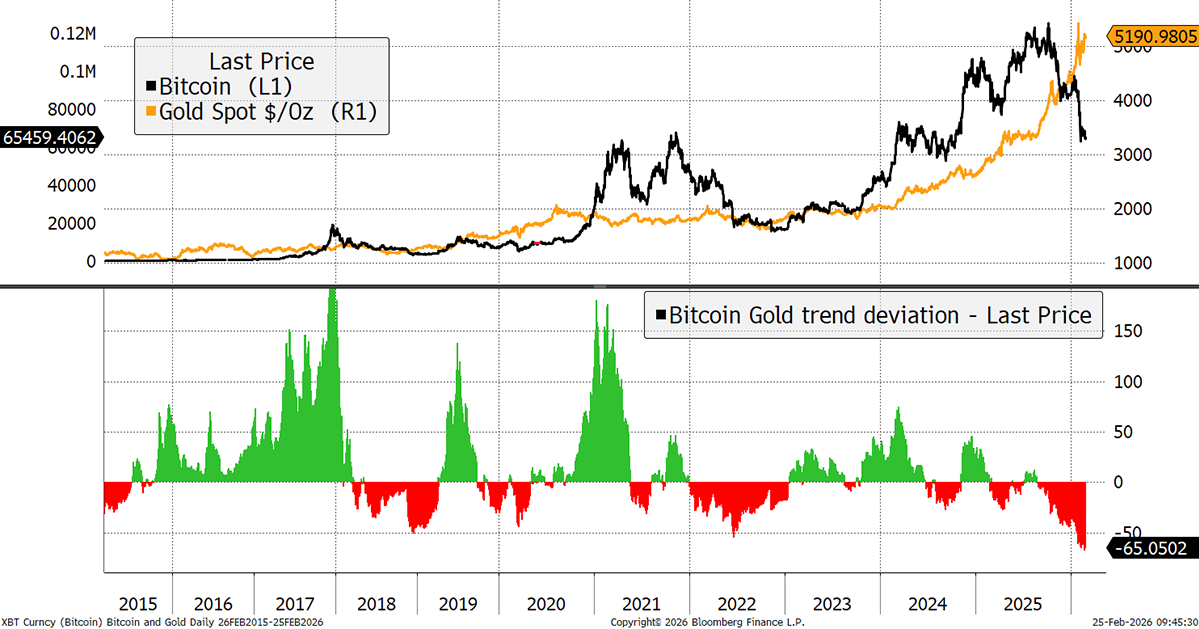

| Crypto Market Review: Volatility Persists Amid Liquidations and External Pressures January 2026 proved challenging for Bitcoin and the cryptocurrency ecosystem, underscoring the asset class’s sensitivity to leverage and macroeconomic shifts. Bitcoin opened the month around $89,000, briefly rallied to $96,000 mid-month, but suffered a sharp 15% drop on January 29, closing near $78,600, a net decline of about 10% for the month. The broader market mirrored this weakness, with Ethereum down almost 18% and total crypto capitalisation slipping under US$3T as gold and commodities hit record highs in a “safe-haven supercycle.” This divergence exposed Bitcoin’s limitations as a defensive asset during uncertainty. A cascade of liquidations amplified the downturn. The month saw multiple billion-dollar wipeouts, which continue to be driven by overleveraged long positions, echoed the flow-on effects from the prior October 10 meltdown, where thin liquidity and forced selling created a vicious cycle. Geopolitical tensions, including U.S. tariff hikes on Europe and renewed U.S.-Iran friction, exacerbated the risk-off mood, pushing investors toward gold, which surged beyond US$5,000 per ounce. Bitcoin has never been this oversold versus Gold in history. Contrarians should take notice. |

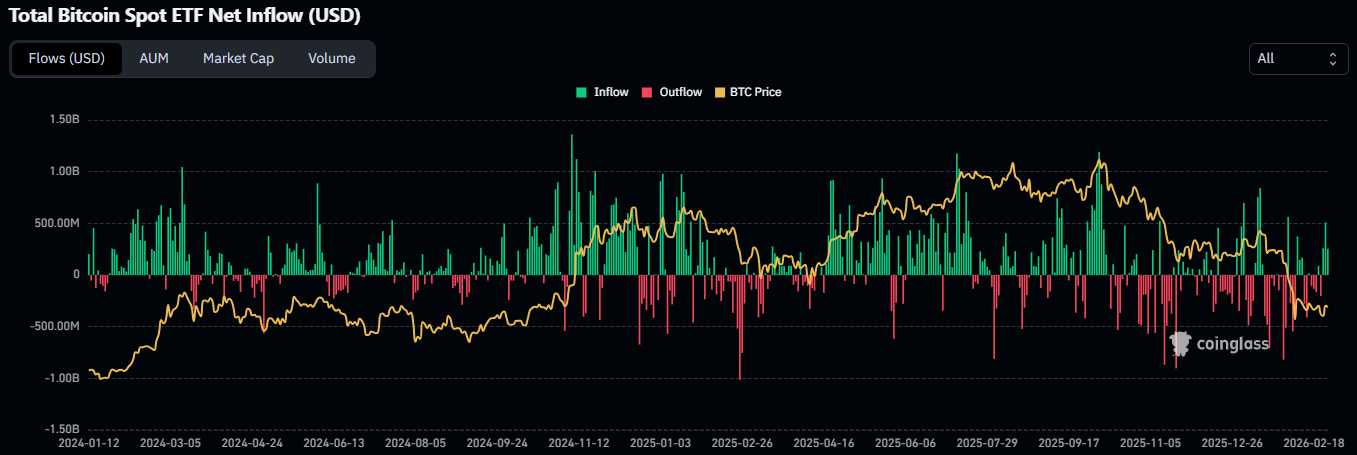

| Quantum computing fears added psychological pressure, though we view them as overstated for now. Estimates suggest up to 7 million BTC, worth $440 billion, could be vulnerable if quantum tech advances sufficiently, including Satoshi Nakamoto’s dormant holdings. However, consensus among experts places a real threat at least a decade away, with current machines far from breaking Bitcoin’s cryptography. Post-quantum upgrades are progressing, but the narrative fueled cautious sentiment, contributing to outflows from spot ETFs, which turned net negative after strong 2025 inflows. |

| The proliferation of synthetic Bitcoin via perpetual futures played a clear role in market weakness. These instruments create leveraged exposure without holding actual BTC, effectively diluting scarcity through rehypothecation and “paper Bitcoin.” Open interest in perps fell from $5 billion to $3.6 billion amid liquidations, but high funding rates earlier in the month encouraged speculative longs that unwound painfully. This synthetic supply—estimated at 3-6x actual BTC—shifts price discovery off-chain, amplifying volatility and undermining Bitcoin’s finite-supply narrative. |

| JANUARY MACRO OUTLOOK: Resilient Growth Meets Persistent Inflation |

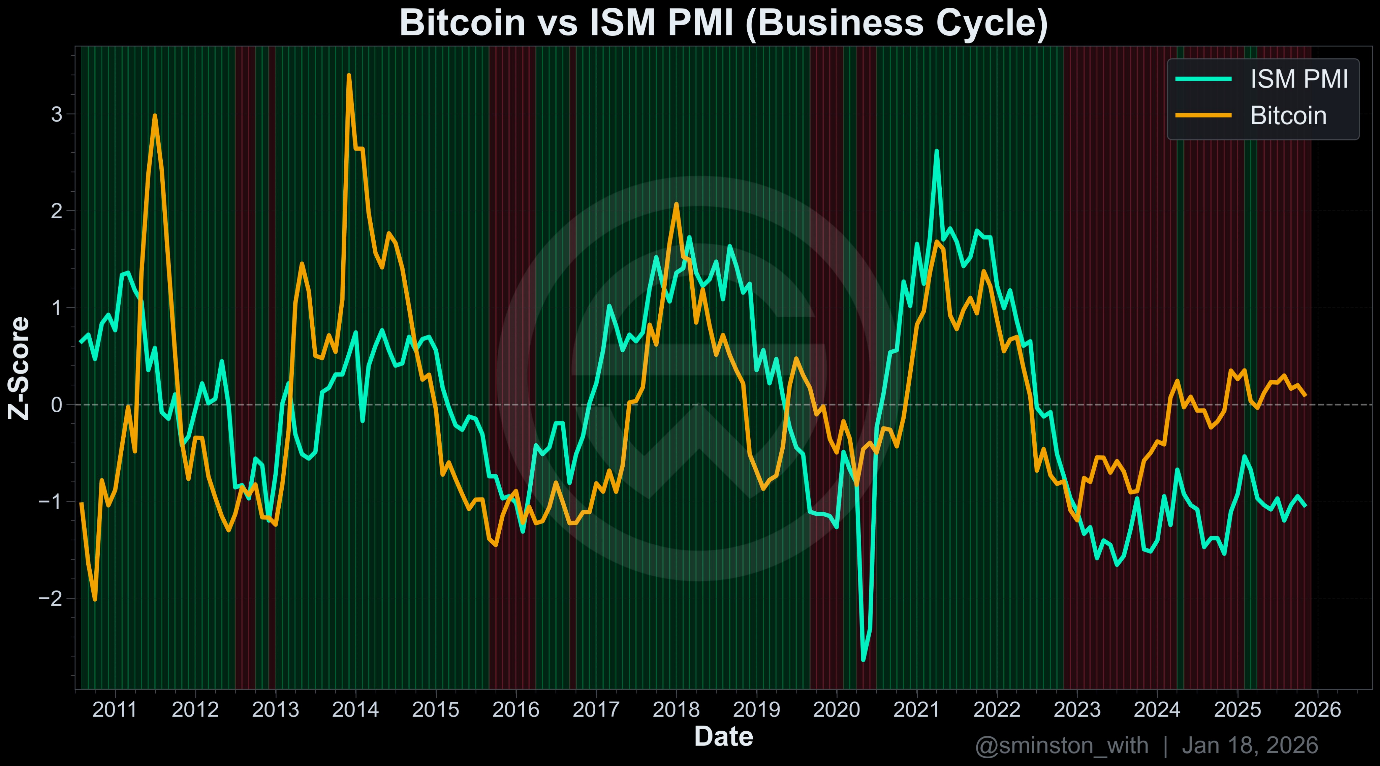

| The global economy entered 2026 on solid footing, with growth projected at 3.3% for the year, steady from 2025 estimates. Accommodative financial conditions persist, despite some volatility in sovereign yields and a brief U.S. dollar recovery. Central banks’ balance sheets remain politicized, with quantitative tightening ending amid reserve pressures, supporting liquidity. In the US, activity expanded at a solid pace, with GDP growth slightly below 2024 levels but resilient. The Federal Reserve held rates at 3.5%-3.75% in January, pausing after three 2025 cuts, citing low job gains, a stabilizing 4.3% unemployment rate, and inflation “somewhat elevated” above the 2% target. Tariffs and fiscal uncertainty, projected to push debt beyond 100% of GDP, could steepen the yield curve, demanding higher long-term premiums. The U.S. PMI composite output index eased to 52.3 in early February flash data, signaling moderating expansion from January’s levels, with services and manufacturing both cooling amid weak demand and high prices. A correlation analysis between Bitcoin’s deviation from its long-term power law trend and the ISM Manufacturing PMI, a monthly survey that has tracked U.S. business performance and conditions since 1948, challenges the halving thesis at its core. The business cycle (the economy’s natural rhythm of expansion and contraction, here measured through the ISM PMI) became the dominant plausible cause for Bitcoin’s price oscillations far earlier than most realize. |

| CRYPTO OUTLOOK: Evolving Dynamics and Early February Turbulence |

| Bitcoin’s “personality” has shifted markedly, failing to live up to its digital gold moniker. In January’s risk-off environment, BTC correlated 0.75 with equities—up from 0.15 in 2021—behaving like a leveraged tech stock rather than a hedge. While gold climbed 13% amid geopolitical strife, Bitcoin dropped 10%, tied to volatility metrics (0.88 correlation with stock vol) and institutional risk algorithms. This identity crisis pits BTC as an inflation hedge, speculative asset, digital gold, or currency—roles increasingly incompatible amid financialization. Declining daily active addresses despite price rallies signal mechanics over fundamentals.Why no safe haven? Leverage via perps and ETFs amplifies downside, while concentrated ownership by institutions and governments heightens volatility. In crises, capital flees to proven stores like gold, not volatile crypto. Early February extended the pain: BTC dipped to $60,000 on February 5 as a flash crash wiped $3.2 billion, the fastest single-day drop in history (-6.05σ velocity) amid tariff uncertainty and weak GDP data. The Bitcoin Fear and Greed Index hit an historic low of 5, Extreme Fear. Rebounds to $70,000 faded quickly, reflecting orderly deleveraging but no capitulation. Looking ahead, we see potential for a bearish 2026 leg, with BTC testing $50,000 lows before catalysts like altcoin ETFs or stablecoin growth ($500B+ market cap) revive sentiment. Regulatory tailwinds, including U.S. market structure bills and quantum preparedness, could stabilize the space. |

Portfolio Update

| The Portal Radiance Multi-Strategy Fund positioned itself in late January to protect from any liquidation event. The increased volatility meant that Deribit’s full-Portfolio Stress Matrix calculated a higher than previously expected worst-case loss scenario. As a result, a decision was made to place a number of perpetual futures sells just below the key US$75k level. The BTC price subsequently continued lower, which would likely have resulted in liquidation had no action been taken to reduce the exposure. However, the unwinding of the leveraged positions effectively ‘locked-in’ the loss, although the Fund was able to replace its linear perps exposure with a defined risk position with convexity via long Calls. What forced the unwinding of the strategy was a structural margin event — not a failure of the directional thesis. The rapid price gap-down due to extreme shocks, an increase in volatility beyond modelled ranges, and leverage amplification caused by the perpetual futures position expanding exponentially overwhelmed the insurance Puts, causing the portfolio margin requirements to rise faster than the Puts gained value. The focus now for the Radiance find is disciplined recovery with a stronger capital structure. We have established a Tripartite Strategic Alliance that will combine AI research, quantitative derivatives expertise, and digital asset structuring to build the Radiance fund in a staged, risk-controlled manner, using a combination of market-agnostic strategies and BTC compounding through directional exposure. The Portal Digital Fund Update The Portal Digital Fund has begun pivoting to systematic, market agnostic, uncorrelated strategies as they deliver consistent performance in every market regime, from harvesting structural premia and recurring inefficiencies that exist continuously and are not impacted by price. These strategies demonstrated the strength and resilience of their market agnostic returns in 2025, delivering on average a net return of 40%+, while the CCi30 was down 33.3%. This was achieved in a systematic, risk controlled manner, with Sharpe ratios averaging just under 2.0. Digital asset markets remain uniquely inefficient, with persistent structural premia across liquidity provision, basis, volatility surfaces, and microstructure that no longer exist at scale in traditional markets. By concentrating on these persistent, market agnostic opportunities, Portal Digital Fund is targeting returns of 35-45% pa (net), with Sharpe ratios around 2.0. This will be in the context of controlled drawdowns of 12–15%, low beta to the crypto markets, and strong capital preservation.PDF plans to complete the pivot to these strategies by July 1 2026. As always, feel free to reach out with any questions or to discuss how our strategies may suit your portfolio. Greg Galton Chief Investment Officer📧 [email protected] | 🌐 www.portal.am This email contains general information only and is not investment advice. Please see the full disclaimer at the end of the report. |